Mortgage Rates Today: Just Dropped Below 6%, Matching Lowest Level Since 2022

Mortgage Rates Today have eased, delivering a meaningful shift in affordability: headline averages are now in the mid- to high-5% range, and recent analysis suggests that a modest 25-basis-point decline could price more than a million additional households into the housing market. This development matters because even small rate moves are having outsized effects on buyer eligibility and refinancing math.

Mortgage Rates Today: Current averages and refinance figures

As of February 23, 2026, the average mortgage purchase interest rate on a 30-year loan stands at 5. 87%. The average purchase rate for a 15-year alternative is listed at 5. 37% in the detailed figures, with a summary later noting 5. 35% for the same 15-year purchase product; both place 15-year options squarely in the mid-5% range. For homeowners considering a refinance, the average 30-year refinance rate is 6. 35%, while the median refinance rate for a 15-year term is 5. 49%.

Context in the coverage highlights that mortgage interest rates fell by more than a full percentage point on average in 2025, aided by a campaign of interest-rate cuts, and have continued to drift lower in 2026 as unemployment and inflation declined. The current stability in late February has produced multiple purchase-rate options under 6%, and there is room for borrowers to find offers closer to 5% by shopping.

This period of relative steadiness is actionable: buyers and homeowners are encouraged to use the lull to gather rate quotes from at least three different lenders to establish a baseline. Homeowners weighing a refinance should crunch the numbers carefully and account for fees and closing costs that can offset monthly-rate improvements.

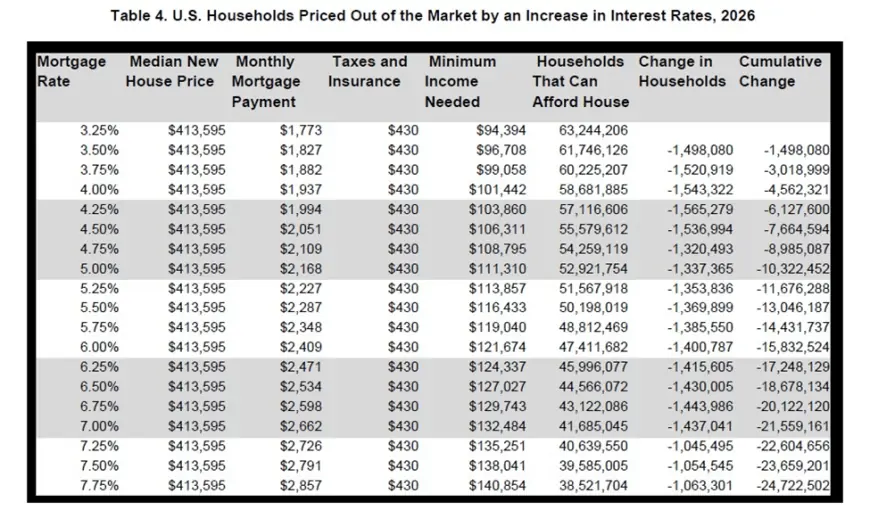

A 25-basis-point decline could price 1. 42 million households into the market

Recent affordability analysis outlines how a modest 25-basis-point move matters materially. At the start of 2026, when the average 30-year fixed rate sat at 6. 25%, about 31. 5 million households could afford a median-priced new home listed at $413, 595, which required a qualifying household income of $124, 336 under front-end underwriting standards.

A decline from 6. 25% to 6. 00%—a 25-basis-point cut—would lower the qualifying income threshold enough to bring roughly 1. 42 million additional households into the pool able to afford that median-priced new home in 2026. The gain in affordable households reflects how many household incomes cluster near key qualification cutoffs; relatively small shifts in qualifying income can therefore unlock substantial increases in buyer pool size.

The analysis further notes that the same 25-basis-point relief at higher rate levels is less powerful: for example, a drop from 7. 75% to 7. 50% would only add about 1 million households. Separately, factoring in lower operating costs from more energy-efficient homes could create payment equivalents that mimic a 75-basis-point reduction, potentially bringing as many as 4 million more households into affordability.

What buyers and owners should do now

- Use the current stability to gather multiple rate quotes—at least three lenders are recommended to build a comparison baseline.

- When evaluating refinance moves, run the math including fees and closing costs so the apparent monthly savings translate to net benefit.

- Buyers who were previously marginally priced out may re-enter the market if rates move a few dozen basis points lower; sellers and builders should account for this sensitivity in pricing strategy.

- Consider broader underwriting shifts—such as factoring in energy-efficiency savings—that could materially change qualifying thresholds for many households.

The current slide below 6% and the modeled effects of incremental rate relief underscore that modest interest-rate changes remain a central driver of housing affordability. Details and offers will continue to evolve, and households considering a purchase or refinance should monitor their own qualifying numbers closely.