Survey Reveals ACA Marketplace Enrollees Face Cost Concerns and Coverage Changes

At the end of 2025, enhanced premium tax credits for ACA Marketplace plans expired after a government shutdown over the policy. Filmogaz.com reviewed a new probability-based survey that tracks how enrollees are responding to higher costs and coverage changes.

Survey and methods

The Kaiser Family Foundation conducted the study in late 2025. The initial sample included 1,350 adults enrolled in ACA Marketplace plans.

Researchers re-interviewed 1,117 people, more than 80% of the original group. The follow-up includes returning enrollees, people who moved to other coverage, and those now uninsured.

Who stayed, who left, and plan switching

Most 2025 enrollees—69%—reported re-enrolling for 2026. Of those, 39% stayed in the same plan and 28% switched plans.

About 22% left the Marketplace for other coverage sources. Nine percent of the 2025 cohort said they were currently uninsured.

Younger adults showed higher churn. Half of enrollees aged 18–29 reported leaving the Marketplace. Fourteen percent of that group said they were uninsured.

Reasons for changes

Costs were the dominant motive for switching or dropping coverage. Eight in ten said price drove their decision.

Seventy-one percent called cost a major reason. Only about a third cited changing health needs as a reason.

Rising costs and affordability concerns

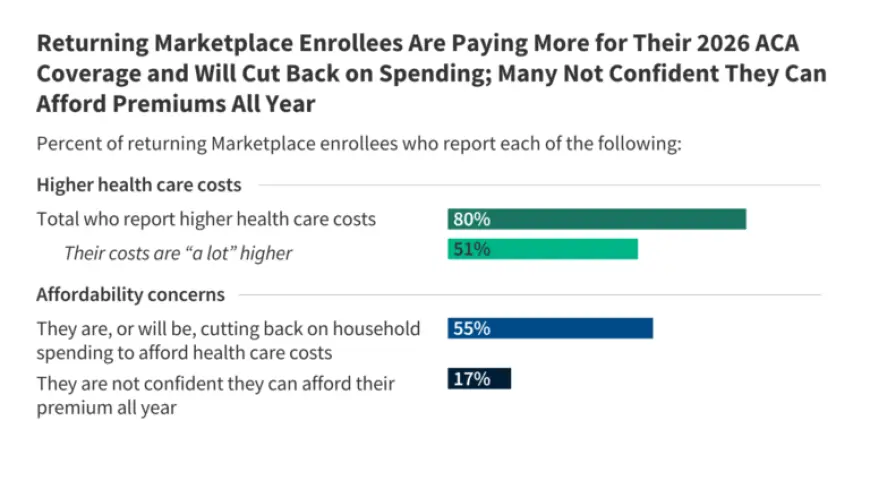

Returning enrollees widely reported higher costs for 2026. Eight in ten said premiums, deductibles, or cost-sharing were higher than in 2025.

Half (51%) said costs were “a lot higher.” Sixty-three percent said premiums rose, and 40% said premiums rose a lot.

Nearly half reported higher deductibles. About a third reported higher coinsurance and copays. Twenty-six percent of plan switchers downgraded their metal tier.

Worries about care and finances

Most returning enrollees expressed cost concerns. Seventy-three percent worried about affording emergency care or hospitalization.

Nearly half worried about routine visits (49%) and prescription drugs (45%). Worry was greater among lower-income enrollees and those with chronic conditions.

Financial strain was common. Fifty-five percent said they were cutting back on food or basic items to afford care. That share rose to 62% for people with chronic conditions.

Forty-four percent said health costs made it harder to pay other bills. Specific pressures included groceries (37%), utilities (32%), rent or mortgage (30%), and transportation (30%).

Many reported coping actions. Forty-three percent planned to work more or take another job. Twenty-three percent planned to delay other bills. Twenty percent expected to increase borrowing.

Coverage stability and payment concerns

Seventeen percent of returning enrollees said they were not confident they could afford premiums for the entire 2026 year. Four percent had not yet paid their first 2026 premium.

Some enrollees remain in grace periods for nonpayment. Those protections may delay, but not prevent, future coverage loss.

Public reaction and political implications

The open enrollment process left many enrollees upset. Sixty-three percent said they felt worried. Fifty-two percent reported feeling angry. Forty-six percent felt confused.

Large majorities blamed lawmakers for the expiration. Seventy-eight percent said Congress did the wrong thing by letting the credits lapse. Ninety-four percent of Democrats agreed, as did 80% of independents and 58% of Republicans.

Who is blamed for rising costs

Returning enrollees placed heavy blame on insurers. Seventy percent said health insurance companies deserved “a lot” of blame for higher costs.

Majorities also blamed President Trump, Congressional Republicans, and pharmaceutical companies. Fewer pointed to hospitals, doctors, or employers.

Effect on voting and civic actions

Health care costs may influence votes. Seventy-three percent of registered enrollees said costs would have a major or minor impact on their decision to vote.

Seventy-four percent said costs would influence which party’s candidate they support. Democrats were far more likely than Republicans to report a major impact.

Many discussed the issue personally. Seventy-six percent talked with friends or family about rising insurance costs. Smaller shares contacted officials (14%) or posted about costs on social media (12%).

The Filmogaz.com review of this survey shows that ACA Marketplace enrollees face cost concerns and coverage changes. The findings highlight potential political consequences and continued financial stress for many households.