Nvidia Earnings Report: Record $68.1B Quarter, $78B Revenue Outlook Lifts Focus Back To AI Demand

Nvidia’s latest earnings update delivered another record quarter, pairing blockbuster Data Center growth with a bigger near-term revenue outlook that keeps attention locked on AI infrastructure spending. The results cover the fourth quarter and full fiscal year ended Jan. 25, 2026, with the earnings release issued after the market close on Wednesday, Feb. 25 (ET), followed by a 5:00 p.m. ET conference call.

Nvidia Earnings Report Highlights: The Numbers That Moved The Story

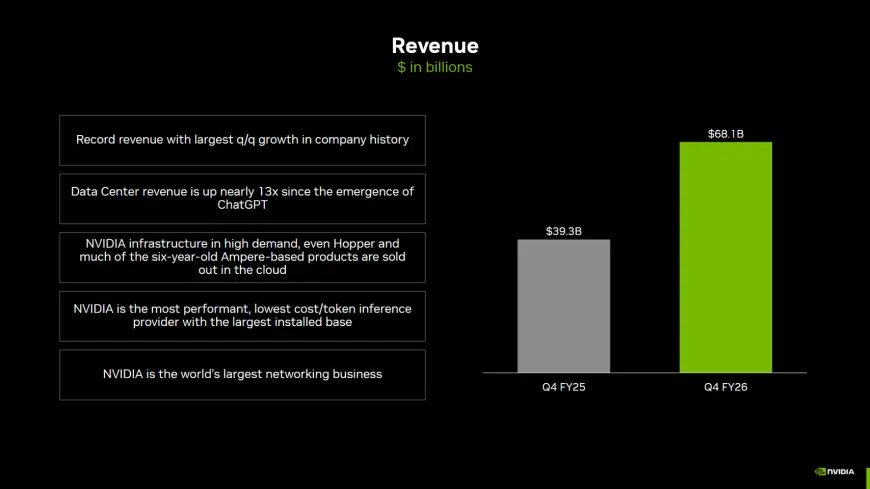

Nvidia posted quarterly revenue of $68.1 billion, up 20% from the prior quarter and 73% year over year. For the full fiscal year, revenue reached $215.9 billion, up 65% year over year. Profitability remained elevated, with GAAP gross margin at 75.0% for the quarter.

Here are the key figures investors and industry watchers are focusing on:

| Metric | Q4 Fiscal 2026 | Change |

|---|---|---|

| Total revenue | $68.1B | +20% q/q, +73% y/y |

| Data Center revenue | $62.3B | +22% q/q, +75% y/y |

| GAAP EPS (diluted) | $1.76 | +35% q/q, +98% y/y |

| Non-GAAP EPS (diluted) | $1.62 | +25% q/q, +82% y/y |

| GAAP gross margin | 75.0% | +1.6 pts q/q |

| Q1 Fiscal 2027 revenue outlook | $78.0B (±2%) | Next-quarter guide |

Data Center Dominance Keeps Driving The Quarter

The quarter’s headline remains Data Center, which generated $62.3 billion—by far the largest portion of company revenue. That growth reflects sustained demand for accelerated computing and AI deployments, with enterprises and cloud operators continuing to build out training and inference capacity.

The scale matters: a quarter with over $62 billion in Data Center revenue signals that demand is not limited to a single customer type or use case. Training clusters remain important, but a growing share of investment is tied to inference—running models in production—where performance-per-dollar and power efficiency can make or break deployment economics.

Guidance Points To Another Step Up, With A Notable China Assumption

For the first quarter of fiscal 2027, Nvidia guided to $78.0 billion in revenue (plus or minus 2%). The company also flagged an important assumption: it is not assuming any Data Center compute revenue from China in its outlook. That framing will keep attention on geographic mix and how demand is distributed across regions and customer categories.

On profitability, Nvidia’s Q1 outlook calls for GAAP gross margin of 74.9% and non-GAAP gross margin of 75.0%, both plus or minus 50 basis points. Operating expenses are expected to rise to approximately $7.7 billion GAAP and $7.5 billion non-GAAP.

A Non-GAAP Reporting Change To Watch Starting This Quarter

One accounting presentation change stands out for anyone tracking trend lines: beginning in Q1 fiscal 2027, Nvidia will include stock-based compensation expense in non-GAAP financial measures. In practice, that can affect how readers compare non-GAAP results versus prior periods, especially for operating expenses and margin math.

For the upcoming quarter, Nvidia expects stock-based compensation expense to have a 0.1% impact on non-GAAP gross margin and to add $1.9 billion to non-GAAP operating expenses. The shift doesn’t change cash generation directly, but it can change how “clean” non-GAAP profitability looks versus earlier quarters.

Cash, Buybacks, And The Shareholder Return Cadence

Beyond revenue and margins, the earnings release reinforced Nvidia’s cash-generation engine. For fiscal 2026, the company reported $102.7 billion in operating cash flow and $96.6 billion in free cash flow, while returning $41.1 billion to shareholders through repurchases and dividends.

Nvidia also ended the quarter with $58.5 billion remaining under its share repurchase authorization. On dividends, the next quarterly cash dividend is $0.01 per share, payable April 1, 2026, to shareholders of record March 11, 2026.

What This Nvidia Earnings Report Signals For The Next Quarter

The biggest takeaway from this Nvidia earnings report is the combination of (1) massive quarterly scale, (2) continued Data Center momentum, and (3) a higher near-term revenue outlook—while also setting expectations for how non-GAAP reporting will look going forward.

Near-term attention now shifts to execution against the $78.0 billion revenue guide, supply delivery timing for new platform ramps, and whether demand broadens further across enterprise adoption and inference-heavy deployments. The next set of results will test whether Nvidia can keep growing at today’s pace while sustaining mid-70s gross margins in an environment where customers are scrutinizing total cost of ownership more closely than ever.