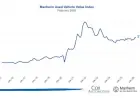

Salesforce Stock (CRM) Slides After Earnings Despite Record EPS Beat — Weak 2027 Revenue Guidance Spooks Investors

Salesforce (NYSE: CRM) delivered its strongest earnings-per-share beat in recent memory on Wednesday, February 25, 2026 ET — but CRM stock still tumbled in after-hours trading as Wall Street zeroed in on revenue guidance for fiscal year 2027 that came in short of expectations. The results mark a pivotal moment for a company already battling a steep 28% year-to-date decline.

CRM Stock Falls 5% After Hours Despite EPS Blowout

CRM stock dropped roughly 5% in extended trading after the closing bell Wednesday, even as Salesforce posted adjusted earnings per share of $3.81 — a massive beat against the consensus estimate of $3.04 to $3.05. That represents a roughly 25% upside surprise on the bottom line, the company's fastest revenue growth rate in two years.

Revenue for the quarter ending January 31, 2026 came in at $11.20 billion, essentially matching the $11.18 billion Wall Street projection and rising 12% year over year. Net income climbed to $1.94 billion, or $2.07 per share, up from $1.71 billion in the same quarter a year ago.

Salesforce CRM Fiscal 2027 Guidance Misses the Mark

The critical pressure point for Salesforce stock was the forward outlook. For fiscal year 2027, Salesforce guided revenue to a range of $45.8 billion to $46.2 billion — implying 10% to 11% growth. The midpoint of $46 billion landed just below the analyst consensus of $46.06 billion, a miss that proved enough to rattle investors already on edge.

Adjusted earnings per share guidance for fiscal 2027 came in at $13.11 to $13.19, with the midpoint of $13.15 landing roughly in line with Wall Street expectations. For the upcoming first quarter of fiscal 2027, Salesforce called for revenue of $11.03 billion to $11.08 billion and adjusted EPS of $3.11 to $3.13.

$50 Billion Buyback and Anthropic Stake Offer a Silver Lining for CRM

Salesforce announced a sweeping $50 billion share repurchase authorization alongside the earnings results — a significant capital return signal aimed at long-term shareholders. The company also disclosed an $811 million gain on strategic investments for the quarter, driven largely by its stake in Anthropic, compared to just $96 million in the prior-year period.

The Agentforce platform — Salesforce's flagship agentic AI product — continued to scale, with the company reporting that its platform processed 11.14 trillion tokens during the quarter. Current remaining performance obligation, a closely watched forward revenue indicator, came in at $35.1 billion, ahead of the $34.53 billion consensus estimate.

CRM Stock Has Lost 28% in 2026 Amid AI Software Selloff

Before Wednesday's earnings, Salesforce stock closed at $185.42 on February 24 ET — already down roughly 28% year to date and approximately 40% below its 52-week high of $308.32 set in February 2025. The sharp selloff in CRM and other SaaS names has been fueled by broader investor anxiety over AI disruption to legacy software business models.

A widely circulated blog post from Citrini Research, depicting a hypothetical "AI depression" scenario in 2028, hit software stocks hard in mid-February. IBM also suffered its worst single-day loss since 2000 after Anthropic published details about Claude Code's ability to assist in modernizing Cobol-based enterprise software — code that many large companies still rely on.

Analyst Price Targets on CRM Vary Widely

Wall Street remains broadly constructive on Salesforce stock despite the year-to-date pain. KeyBanc maintained an Overweight rating on CRM while cutting its price target to $300 from $400, citing compressed market multiples. Morgan Stanley, also equivalent to a buy on the stock, trimmed its target to $287 from $398 but emphasized conversations with channel partners suggest the company is in "early innings" of its AI monetization cycle.

BMO Capital Markets holds an Outperform rating with a $235 target, while UBS carries a Neutral rating and a $200 target. The consensus rating across analysts tracked by MarketBeat sits at Moderate Buy, with an average price target of $304.33 — implying significant upside from current levels if the Agentforce growth story continues to take hold.