Palantir Stock Draws Wall Street Upgrades After Early‑Year De‑Rating

Analysts have shifted their stance on palantir stock following a swift contraction in forward valuation multiples in the opening weeks of 2026, and one major firm has moved to upgrade the shares. The change matters now because the reassessment ties a lower risk profile to rising AI product demand and accelerating revenue trends.

Development details — Palantir Stock upgrade

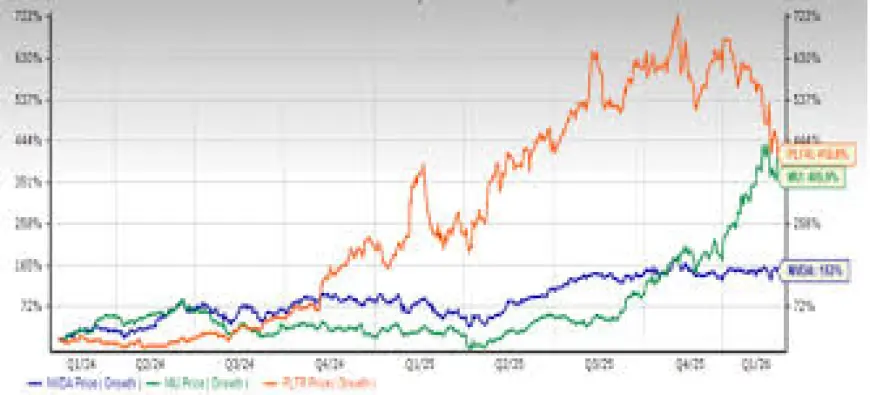

On February 18, Mizuho analyst Gregg Moskowitz raised his rating on Palantir Technologies Inc. to Outperform and set a price target of $195. Moskowitz and his firm pointed to what they called a "category of one" business profile, driven by revenue growth, expanding margins and accelerating performance at scale. A central numeric driver of the upgrade was a 46% contraction in Palantir’s estimated 2026 enterprise value‑to‑free‑cash‑flow multiple during the first six weeks of the year, a move Mizuho framed as having materially de‑risked the stock’s valuation.

Market performance has already been notable: over a two‑year span Palantir’s shares climbed by roughly 412. 6%, outpacing several peers in the AI and data infrastructure space. That price performance has coincided with rapid product adoption in both commercial and government channels.

Context and escalation

Palantir’s business momentum has been driven by demand for its software platforms and its Artificial Intelligence Platform (AIP). The company’s U. S. commercial segment reported $507 million in fourth‑quarter 2025 revenue, a 137% year‑over‑year increase and a 28% sequential rise. Government revenue in the same quarter reached $570 million, up 66% year‑over‑year and 17% quarter‑over‑quarter. Those concrete results underpin the valuation debate that unfolded in early 2026: as multiples contracted, analysts re‑weighed upside against a lower entry multiple.

What makes this notable is the interaction between the selloff and the underlying operating results: the multiple compression created a smaller gap between current valuation and the company’s revenue trajectory, prompting at least one major analyst to conclude the risk/reward has improved.

Immediate impact

The upgrade and the valuation reset have immediate market and investor implications. The Mizuho action provides a new benchmark for institutional investors weighing Palantir exposure, anchored to a $195 price target and the firm’s assessment of reduced downside risk after a 46% multiple contraction. For corporate stakeholders, the boost in analyst sentiment reinforces the commercial traction of Palantir’s platforms — Gotham, Foundry and AIP — which the firm cites as offering limited direct competition and more predictable cash flows.

Clients and potential enterprise buyers face the practical consequence of stronger vendor momentum: Palantir’s reported remaining‑deal values and large sequential jumps in commercial revenue signal material pipeline conversion, which can translate into more predictable revenue recognition over coming quarters.

Forward outlook

Palantir has provided revenue targets that reflect the company’s confidence in continued adoption. The firm expects full‑year 2026 revenue to more than double to a range between $7. 182 billion and $7. 198 billion, up from $3. 320 billion in 2025. The U. S. commercial segment’s remaining deal value reached $4. 38 billion in the fourth quarter of 2025, representing a 145% year‑over‑year increase and supporting the near‑term revenue roadmap.

Key milestones ahead include continued quarterly revenue reporting that will test whether the sequential and year‑over‑year gains in late 2025 persist through 2026. Analysts who have adjusted ratings are watching how the combination of a lower entry multiple and accelerating top‑line growth plays out across upcoming earnings and guidance updates.

In short, the early‑2026 valuation contraction altered the investment calculus and opened the door for renewed analyst optimism, anchored by concrete revenue acceleration and a stated full‑year 2026 revenue target that more than doubles the prior year’s sales.